EXL Paymentor℠ FAQs

Largely, there are 4 key problem areas we see in collections and specifically early stage collections, today. These are:

a. Inability to segment debtors by persona and value-at-risk

b. Minimal use of customer self-service portals

c. No segment-based tones for messaging

d. No behavior-based tone progression

e. No expedited collection paths for certain customers (e.g. asset sale, 3rd party collection)

a. No pre-delinquency prediction

b. External customer-data is not used extensively for modeling purposes

c. Customer interaction / behavior data is not leveraged

d. Machine learning techniques not used to predict customer response

e. Inability to define optimal channel, optimal time and optimal frequency of customer contact

a. Little use of digital or omni-channel communication

b. Low call center/agents efficiency as these are “tough conversations”

c. Little integration between phone, email, text and website

d. External data not in use for skip tracing activity

a. Minimal use of cloud based solutions that can scale efficiently

b. Customer Self-service portal are not in place in most cases

c. Inability to restructure debts digitally

d. Inability to collect payments digitally

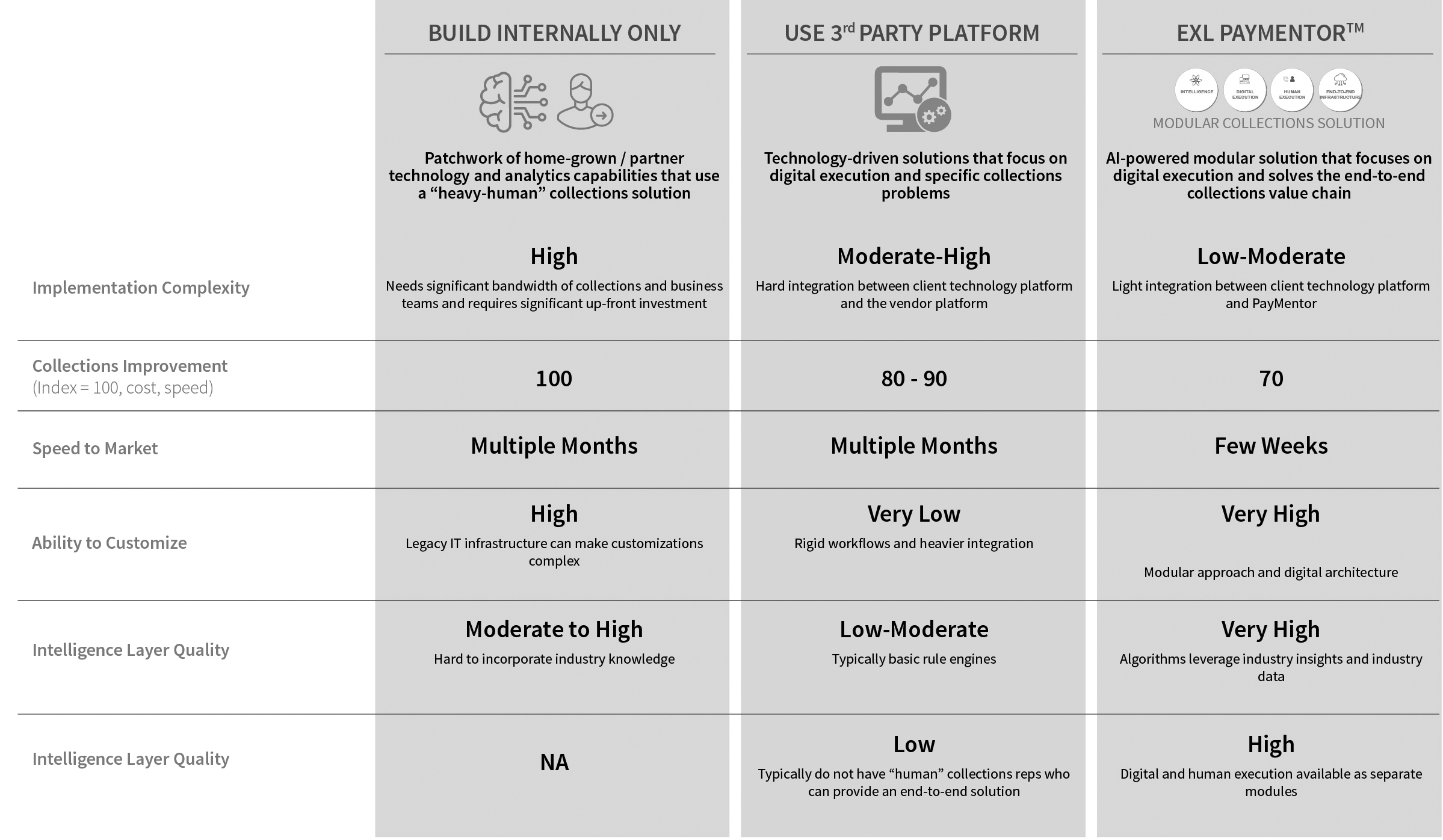

Typically, collections has always been a neglected part of the lender’s business strategy with the majority of investment being made in sales, marketing and service. There are three types of approaches we have seen in the market:

Smaller lenders, instead of improving their in-house collections, place their portfolio or even sell it to the agencies at an early stage, which results in an accelerated credit loss recognition, increased cost of funds, and in most cases worsens customer experience

Minority of the big lenders (minority today) don’t see the root cause of their poor collections results clearly and try to compensate by increasing the intensity of contact via the phone (or even augment it via digital contact). This strategy increases costs, has limited headroom for improvement / scaling due to the regulatory guardrails and worsens customer experience.

A majority of big lenders understand the issues well but don’t do a holistic job of solving for all 4 problems outlined in question 1. They typically take a piecemeal approach by either investing in collections analytics including customer segmentation or by only solving for channel of communication by the use of text, email, SMS and a customer portal. Very few lenders do all four things together i.e. a) improvement of intelligence / analytics, b) use of digital execution channels, c) updating of IT infrastructure and d) developing a seamless omni-channel experience for the customer.

There are 3 options to help companies improve their collections’ outcomes:

- Develop in-house collections capabilities;

- Other 3rd party collections platform;

- Go with EXL Paymentor℠

Below is a comparison of EXL Paymentor℠ with the other two options available

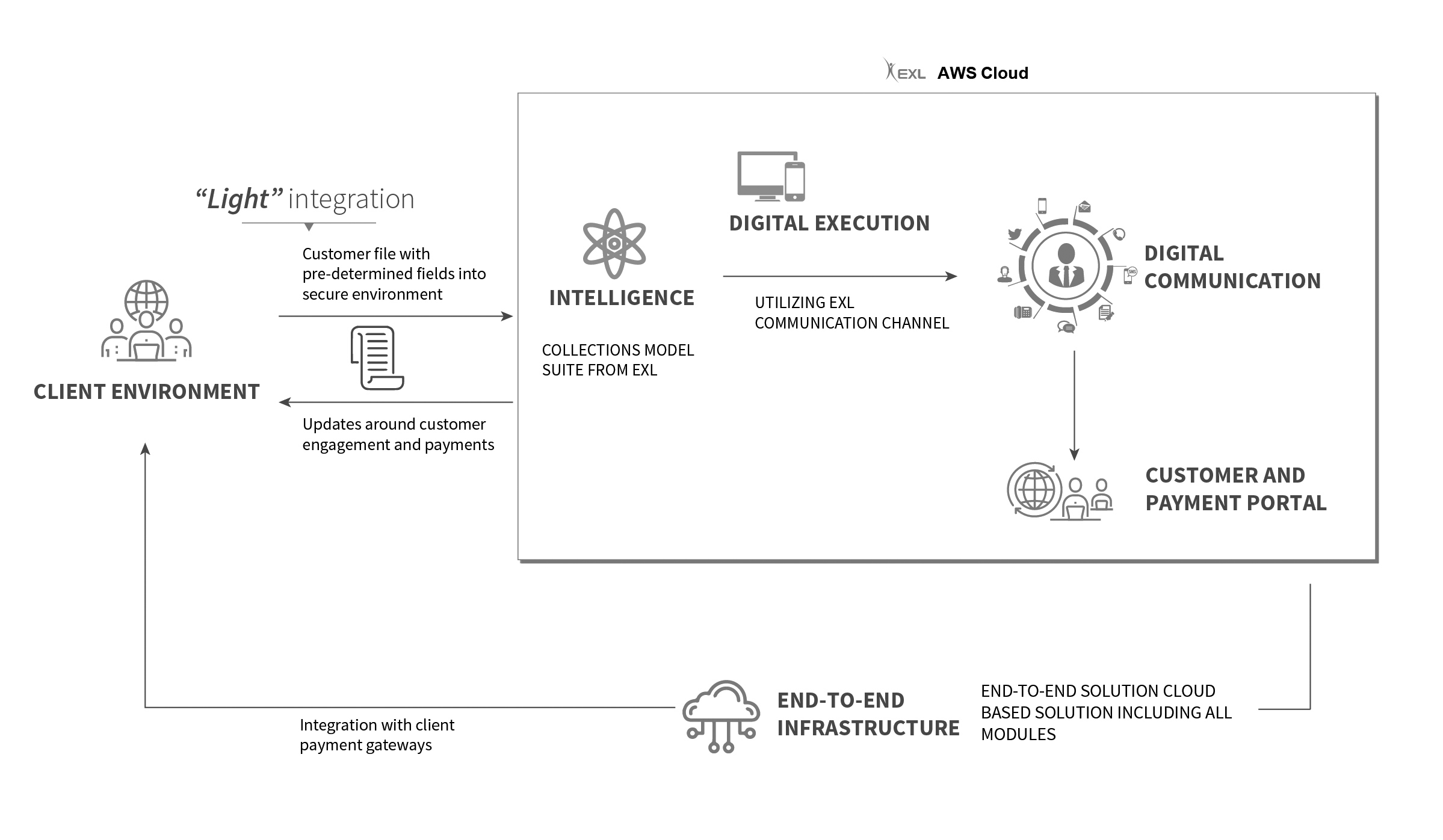

EXL PayMentor was designed specifically to be able to do the whole-cycle digital debt collections, but our biggest strength is the modularity of our solution which allows us to customize it and implement quickly.

As the first step, the EXL PayMentor team analyzes the client’s data to assess the scale of their collections problem, by using industry benchmarks that we have developed using a combination of proprietary and partner data.

Next, the EXL team discusses the findings with the client and proposes a solution that optimally combines our 4 modules. (The 4 modules are a) Intelligence / analytics, b) Digital Execution, c) Cloud-based infrastructure and a client portal and d) Integration with “human” phone channel to drive omni-channel experience)

After the client agrees with the solution design in principle, EXL can propose one of two implementation models; a) The modules stay on the cloud instance of EXL, or b) The modules are deployed within our client’s infrastructure (or their cloud)

Based on the implementation model that the client proposes, we offer 2-3 types of commercial constructs to them:

i. They consume this as collections-as-a-service where they pay $1-2 per account that is placed with EXL PayMentor. This assumes that they leverage the solution built on EXL’s cloud instance

ii. We build the collection solution in their cloud (or on premise) infrastructure which has an upfront build cost (which is significant), but after that the client runs the solution with no maintenance by EXL

iii. We build the collection solution in their cloud (or on premise) infrastructure AND also do maintenance. In this scenario, our upfront build cost is lower and we charge a monthly maintenance fee

The starting tone is defined purely based on a multi-dimensional score card, which is a combination of several modeling inputs. However, that’s just the starting message. The tone of the next message is driven by the customer’s behavior, which in addition to the payment history and the financials comprises over 30 different criteria. Here are 5 examples of such criteria:

- Was the last message received and read?

- Did the debtor visit the self-service portal, and did he see the screen with the payment options proposed?

- What was the tone of the previous message?

- What is the reason for delinquency?

- What’s the most optimal payment option for the debtor?

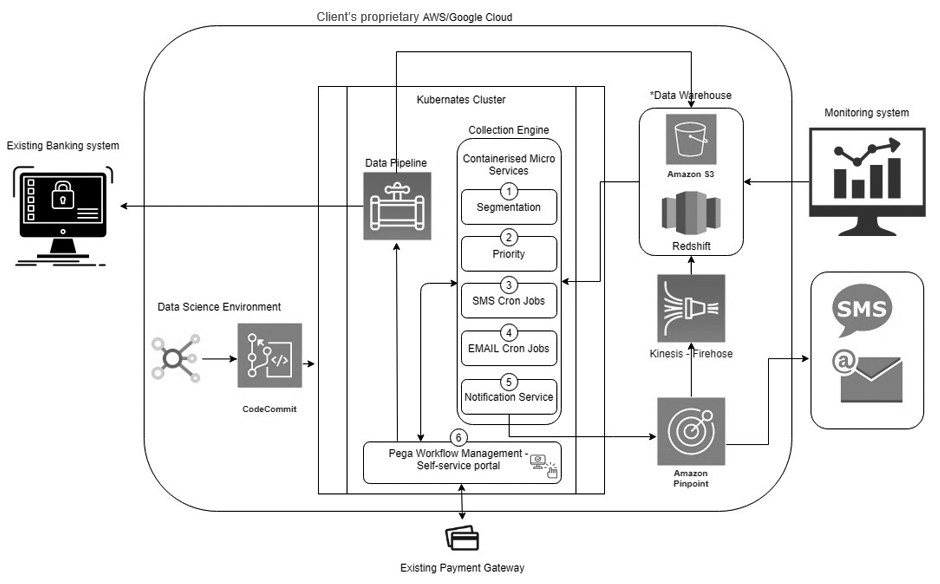

Even though each implementation is uniquely tailored to tackle our client’s needs in the most cost-efficient and least time-consuming manner, these are the architecture diagrams of 2 most popular engagement models, namely:

- EXL PayMentor as a service: the solution is hosted on EXL’s cloud instance and is consumed by the client as a managed service (see chart 2 below);

- EXL PayMentor built in the client’s infrastructure: the solution is built in the client’s cloud-based infrastructure (see chart 3 below)

Chart 2: EXL PayMentor™ as a managed service, hosted on EXL cloud

The key functionalities in our “standard” solution include:

- Intelligence module:

- o Customer segment (based on our experience) collection models using machine learning techniques, such as reinforced learning;

- o Communication strategy with corresponding message templates for different digital communication channels;

- o Treatment and debt restructuring options, e.g. pre-defined payment plans, build-your-own payment plans, grace period-based payment plans, forbearance offer, settlement offer.

- Digital Infrastructure module: Self-service portal that enables a virtual dialogue and instant back propagation of data, digital channels with detailed end-point deliverability statistics, BI-enabled MIS and multiple micro-services and APIs for easy data integration;

All these components are set up in such a way that it takes no time to customize them for our clients’ specific needs.

Integration with “Human” contact center is not available in “plain vanilla” version but we have the Ability to quickly develop or integrate with agent screens and an auto dialer to enable live calling (see question 9).

It depends on the engagement model and amount of customization needed

- The integration may take as little as 4-6 weeks, if the solution is hosted on EXL cloud, needs little customization to the intelligence module and will be managed by EXL as a service.

- If we talk about building a collections solution for our clients, which requires a custom installation on the client’s server to incorporate our client’s existing collections infrastructure, it will take longer, around 14-20 weeks.

Three scenarios for integration are as follows:

1. EXL Paymentor is hosted on EXL’s cloud infrastructure and the client’s phone collections platform is in their local environment:

a. We can create a data-pipe or data connection with a client’s dialer / telephony infrastructure. All important information, including the contact data, modeling outputs, self-service portal data captures and the segment tags can be transferred from EXL PayMentor to the client’s legacy collections platform via file transfer on a daily (or predetermined) frequency to prevent contacting the debtors who have already paid.

b. The data from Paymentor will need to be consumed by the client’s collections platform and the client’s dialer in addition to being available to their agents on their screen.

2. EXL Paymentor and the client’s collection platform are within the client’s environment:

a. In this case there is a “heavy” integration between EXL Paymentor and the client’s collections platform including their auto dialer

b. Our ‘intelligence’ solution can be the omni-channel “orchestrator”, which decides which channel to use for which customer and at what frequency and tone to prevent contacting the debtors who have already paid.

3. EXL Paymentor and the client’s collection platform are deployed on EXL’s cloud environment:

a. EXL Paymentor decision engine is integrated with the client’s legacy auto dialer, if any, or EXL leverages its own auto dialer and the solution used as a single point of orchestration across all the communication channels, both digital and a phone channel.

b. The operators will be working via EXL Paymentor agent screens, which will be customized as per the client’s requirements.

EXL partners with several lending clients to create real, measurable value through operations outsourcing services including loan origination, servicing, default management and debt collections. We help clients build intelligent operations by deploying advanced analytics, AI, robotics and other domain-specific technology solutions.

Key facts about EXL in BFS are:

17+ Years of strong knowledge of BFS Ops & Analytics

8 Of the top 10 US banks partner with EXL

3 Of the top 5 banks in UK partner with EXL

8 FinTechs and alternative lenders

1. Data knowledge:

a. 6000+ data attributes on 244M+ individuals in US

b. Extensive experience of working on external data – e.g. bureau, skip tracing, bankruptcy etc.

c. 17+ Years of strong knowledge of BFS Ops & Analytics

2. Extensive experience in collection modelling and strategy

a. Collection modelling and strategy partner for 2 out of top 5 US Credit Card Issuers, 3 out of top 5 UK banks and multiple FinTechs and alternative lenders:

i. Early and late stage

ii. Contact strategy – channel, time and frequency optimization

iii. Treatment optimization

iv. Call center operation optimization

v. 50+ periodic MIS reports for collection

3. Operations Expertise

a. Managed collection operations for globally known lenders:

i. Top 5 UK bank

ii. Leading P&C insurer

iii. Fortune 50 Insurance and Financial services provider

iv. Leading global energy company

4. Partnership ecosystem

a. Partnering with Verisk/ Argus on the US consortium data;

b. Collaborating with Credit Bureaus and 3rd Party Data providers

Here is what the top 3 analyst firms say about EXL and EXL PayMentor:

a. Niche in Gartner Magic Quadrant for Data and Analytics Service Providers (2020)

b. Leader in IDC MarketScape: Worldwide Analytics for Business Operations Services 2019 Vendor Assessment

c. Featured in HFS Top 10 Banking and Financial Services Sector Service Providers, 2019

EXL Paymentor is a payment assistance solution and covers a wider range of functionality than a debt collections solution does: it manages both debt collections and customer experience.

Digital collections by EXL Paymentor does not replace, but augments the phone channel:

- It improves the customer experience through a well-thought communicating strategy, which can only be controlled via digital (human is prone to deviate from the script);

- It improves the connection rate through a better-determined communication channel;

- It lowers the cost to collect through replacing some of the dialing attempts with cheaper ways to communicate (e-mails, SMS, IVR), but only when it doesn’t sacrifice the collected amount.