IFRS 17: Achieve Benefits beyond Compliance

After a gestation period of more than 20 years, the International Accounting Standards Board (IASB) published its new accounting standard for insurance contracts in May 2017. Since then, there have been multiple amendments with a final amendment to IFRS 17 accounting standard, once-in-a-lifetime regulatory change confirmed in June 2020. At this stage, the uncertainty that has clouded its implementation has now been eliminated. But the entire implementation cycle has not been and is not going to be a smooth sail. The challenges are compounded by another once-in-a-lifetime event, the pandemic. Although the industry can take solace from the revised go-live date being pushed to 1 January 2023, there are several “if’s, but’s and how’s” that are still being explored.

Foreword

This paper is targeted to small- and medium-sized organisations who are still at a nascent stage of IFRS 17 implementation. The paper objectively analyse varied options that can be adopted depending upon the organisation’s risk and budget appetite. Also included is the ideal journey a company should take in light of the revised timeline by IASB to go-live on 1 January 2023.

The analysis provides an industry perspective and details of where the selected enterprises from diverse quadrants of the insurance industry stand as of now and at which stage of implementation they ideally should have been.

The study looks at a blend of organisations that are at the beginning or in the middle of their journey but struggling to move ahead due to varied constraints. This pit stop provides them with an opportunity to analyse their current state and plan effectively for a better way forward. Matters to be considered for a good plan include:

- The fast-approaching timeline

- Stage of implementation

- The way forward with implementation

- Implementing best practices

- What to expect post go-live

Implementing IFRS 17 requirements involves major changes across finance, data, actuarial, systems, as well as in investment assets per IFRS 9. All these areas have major interdependencies and to keep them in sync throughout the implementation phase is going to be a monumental task. An effort of this scale has significant impact on implementation costs for most insurers. Again, owing to the pandemic the cost of implementation may get impacted depending on the current stage of the project.

The Timeline Is Approaching Fast

At inception, the change to IFRS 17 generated a lot of anxiety. After the IASB passed several amendments, the final version is now set. This has created stability within the Industry as to what exactly will change within the accounting standard and which areas will be impacted. As a result, insurers can now:

- Refine technical interpretation of key accounting policies and draft technical accounting paper

- Baseline business and technical requirements and validate BRDs

- Focus on implementation with pace and certainty

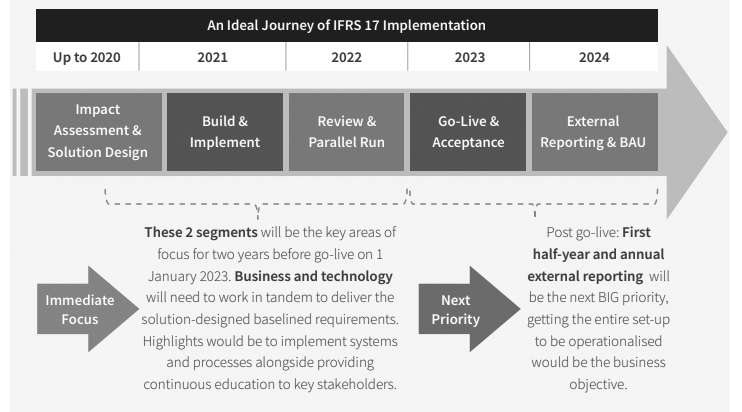

In light of the new timeline, organisations need to define where they are currently and whether their implementation stage is in sync with the regulatory timeline to achieve appropriate compliance. Management should have a clear view of their ideal implementation timeline to access progress

Implementation Stages Driven by Regulatory Timelines

Have ‘started but struggling’ - At this stage, project teams may not be aware of available foundation solutions in the market that can provide optimal outcomes with minimal disruption at a sensible cost. Depending on capacity and budget, such companies may do well adopting a minimum viable product approach

However, ‘early starters’ with deep finances should leverage IFRS 17 change to implement full transformation

Where Are You in the Process?

Time is running out, now that IASB has firmed up the go-live date of 1 January 2023, there are essentially less than two years to grind through the implementation programme. However, some firms are still lagging.

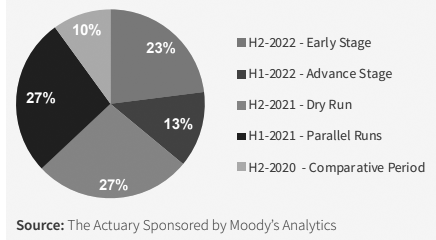

A global study conducted among insurers shows the status of IFRS 17 Implementation and standing of insurers after the deferral was announced by IASB in March 2020.

IFRS 17 READINESS BY

The survey provides a view on IFRS 17 preparedness. It aims to capture a sense of the implementation progress made until the end of 2021. IFRS 17 is principles-based and many firms have yet to settle on their final methodology. A common theme is that firms will try to bring in synergies with other existing processes where possible or combine IFRS 17 implementation with other organisational initiatives. In line with what was expected, the survey indicates that workstreams related to the building blocks of implementing IFRS 17 are mostly set in motion with many firms making significant progress.

Firms still have much to do before progressing on to other aspects of implementation, such as preparing a business plan based on IFRS 17. Most respondents have yet to recalibrate KPIs under standard.

Covid-19 is having a significant impact on resources and implementation schedules, namely:

- Resource capacity - increased demand on already scarce resources in response to the pandemic, such as accountants and actuaries, may have reallocated IFRS 17 resources to other projects

- Infrastructure capacity - new ways of remote working have challenged IT departments, diverting capacity from system, storage and network activities initially reserved for IFRS 17 and IFRS 9 projects to other more urgent initiatives to mitigate the consequences of COVID-19

- Covid induced new norm of working may have an impact on the need for easier access to suppliers in these projects, which may reduce the efficiency of day-to-day operations

- Company’s sstressed financial and solvency positions putting pressure on costs and budget allocations for implementing IFRS 17 and IFRS 9

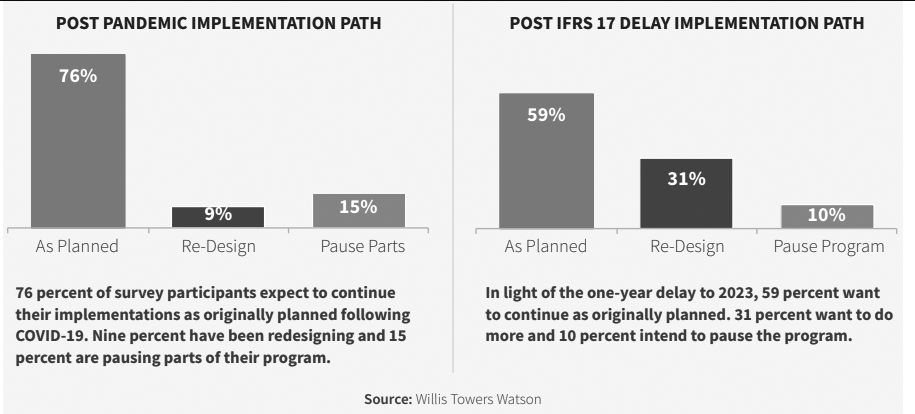

The COVID-19 outbreak significantly increased the need and importance for agile design techniques to ensure that progress can continue as planned and that the overall implementation plan is frequently reviewed as the situation evolves.

Those who were already implementing plans in waves are using the additional time to plan further system developments, tests, data preparation, parallel runs and user training

However, for insurers that are still at an early stage, our advice is that they should accelerate projects without delay due to the complexity of the change.

As of 2021, many companies are still in the process of contracting technological suppliers, whether for the actuarial, accounting or intermediate component.

So, where are you today?

Many insurers who want to be ready a year in advance may perform dry runs over their 2020 financial statements. Others may opt for a “big bang approach” and wait until the last moment. Whatever the strategy, there is a trade-off between certainty and cost.

Either way, no insurer big or small should wait. When it comes to IFRS 17, not acting means moving backwards. DON’T DELAY.

The Right Path to Implementation

Bring Together the Implementation Building Blocks

Compliance with IFRS 17 is an enterprise-wide initiative that cuts across actuarial, risk, finance, IT and other lines of business. It is therefore important to have a clear strategy with a well-defined governance structure to ensure a smooth rollout. An efficient implementation will require establishing explicit business requirements and changes enabled by equally efficient technology and system infrastructure supported by strong data management capabilities.

Understand the Challenges in Implementation

The scale of what needs to be done to comply with IFRS 17 is underestimated by many companies. As companies delve deeper into implementation, they realize that it is more and more complex and has broader operational implications than they originally anticipated. This is true of any big implementation project. Specifically, with IFRS 17 the areas with major challenges include:

- IFRS-Ready Resources - Experts from different teams such as actuarial and finance need to come together, where in-house capacity for such resources is limited.

- Pandemic - The primary focus of insurers was on customers. Pandemic has altered both our economic and health environments, shining the spotlight on safety and resilience.

- Data Estate - Multiple source systems add to complexity in building data feeds to the IFRS 17 data warehouse, and establishing integration with legacy systems can be intricate.

- Disruptive Technologies - Build vs buy or legacy vs new system decisions may impact the plan, solution design, time, scope and budget.

- Interdependencies - Technology and business teams need to work together for seamless implementation.

Coordination among all organisational teams involved in an IFRS 17 implementation is essential. Finance, operations, actuarial and IT teams are the main pillars bearing project responsibilities.

Teams involved need to be highly focussed on areas requiring major changes, which include data sourcing, management and analysis, process re-engineering, finance and accounting, compliance and technology infrastructure. These areas represent the IFRS 17 implementation building blocks.

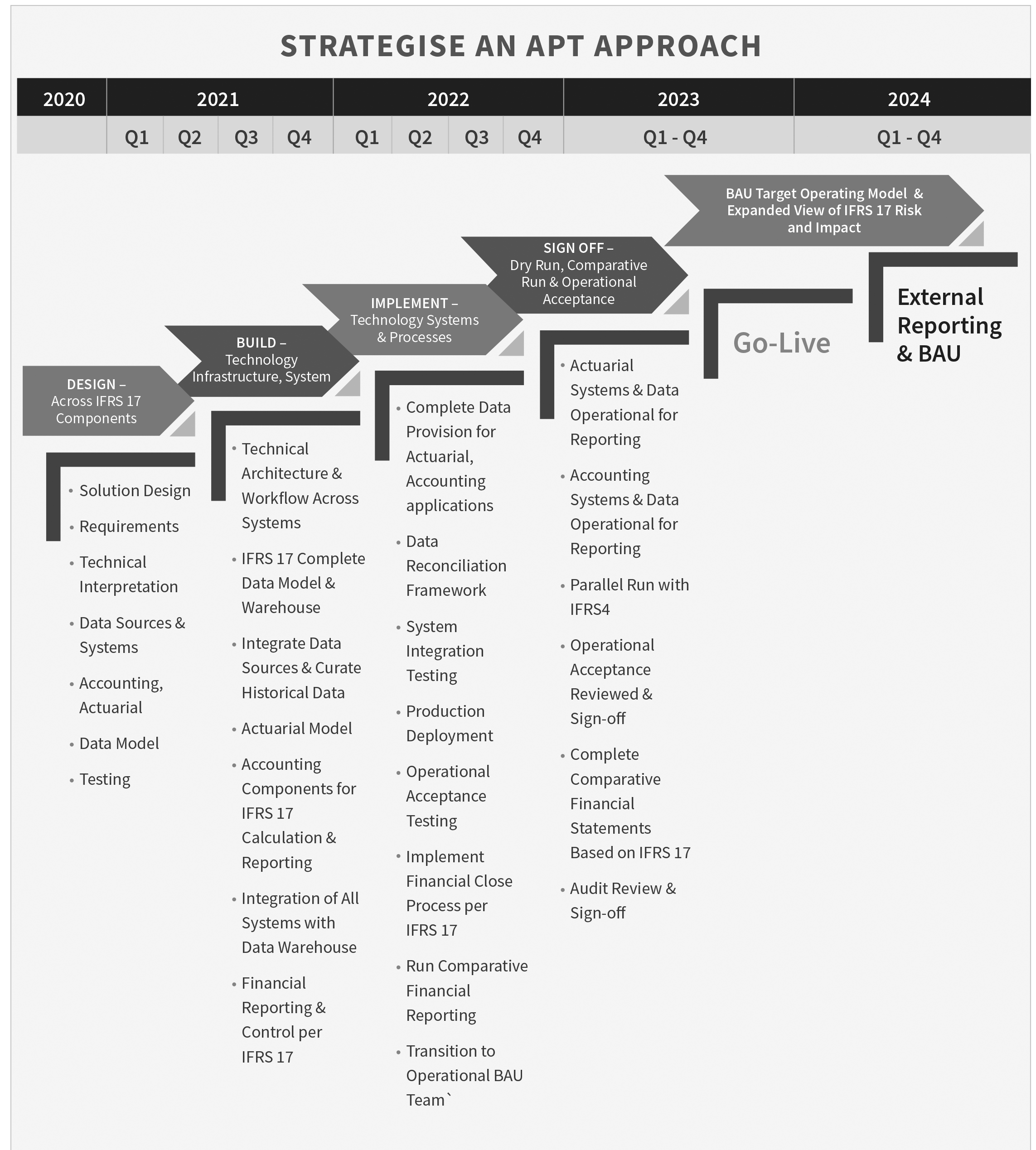

Strategise an Apt Approach

With an effective date under two years away, insurers need to start acting now and refocus their efforts to embrace the change brought about by IFRS 17. The challenge is clear. Insurers should be in the process of implementation or nearing completion of build stage with drafts of technical architecture, data models, data warehouse, actuarial models, as well as finance, accounting and reporting structures set for IFRS 17. The next 1.5 years should be focused on finalising build stage outputs, extended implementation, dry-run and sign-off with a buffer for change control and iteration planned in. These 1.5 years are going to be critical. The clock is ticking and the Implementation will not be smooth, presenting many interdependencies and moving parts to meet ever- evolving requirements.

Implementation Accelerators

Following the agile way of implementation can significantly outstrip other approaches in fully implementing the structural and systems elements of the new operating model for IFRS 17 guidelines. Agile finance leaders are also far more likely to have fully implemented cloud-based enterprise performance management and emerging technologies to support the implementation.

- Create cross-functional integrated teams: Focus work streams with detailed and clear milestones for accounting, actuarial, solution design, data management and engineering, testing, etc.

- Identify and establish different phases of implementation: Assign the scope of deliverables for each work stream within the defined phase.

- Identify key challenges: Establish the ‘to do’ list right now

- Get feedback from dry runs: Depending on stage of implementation, what issues have arisen and how are you addressing them?

- Level of data challenges: Formulate solution leveraging existing IT and data infrastructure

- Communication: Translate complex processes and challenges across all departments.

- Identify, establish and communicate the interdependencies: Across all work streams.

- Leverage external vendor providing core IFRS 17 systems: For late starters or small organisations with limited budgets.

- Leverage shared service center: For key processes.

- Be proactive: Using digital and analytical capabilities to harness the full benefit of the implementation.

- Follow agile and scrum methods to accomplish deliverables: Avoid waiting for all requirements to finish before starting data warehouse design, modeling developments, etc.

- Start with minimum value product: Keep enhancing the design and build as progress is made.

- Have daily scrum meetings to identify challenges and risks: Assign owners to head off risk and maximize value.

- Create a centralised program management office: To support end-to-end implementation.

Businesses must grasp developments in technology and drive agility to develop and implement IFRS 17 strategies promptly when threats or opportunities arise.

The key is to remain nimble in managing the on-going implementation, constantly adapting and innovating to increase stakeholder value.

Bottom Line: Act Now

The IASB’s decision to delay IFRS 17 by a year allows the industry time to plan strategically towards compliance as follows:

Prepare for New IFRS 17 Business as Usual Status by 1 January 2023

Transitioning to business as usual (BAU) will be extremely critical as any compliance failure in external reporting can have serious regulatory, legal and brand reputational consequences. Some of the key issues to address will be:

- Moving to BAU target operating model

- Optimising closing processes

- Understanding the wider business impacts on pricing and underwriting

- Preparing processes and systems for the BAU stage

- Resource requirements

- Skillset/size of teams

- Internal vs outsourcing considerations

- Structuring a training programme

- Managing knowledge transfer

BAU Factors to Consider during Implementation

IFRS 17 implementation requires an exhaustive approach with extensive changes to technology, actuarial and accounting and reporting functions. Therefore, it is crucial to have the right technology and people in place, including those who will work on and manage the implementation. It will take an intense and immense knowledge build-up to move from project to BAU and continue operating successfully. Here’s what to consider:

- Actuaries, accountants and IT analysts working closely together

- Extensive cooperation between actuaries and accountants

- Experienced resources in place to manage the closing calendar in light of IFRS 17 challenges

- Well-rehearsed finance team to provide continuity in reporting

It is imperative that all team members be invested and involved during implementation to make the BAU transition smooth and efficient. Educating the team on IFRS 17 requirements, organisational strategy and the implementation process early will help control costs and minimize delays en route to a successful IFRS 17 transition and future operating state.

How Can EXL Help?

EXL Consulting practice has deep expertise in the insurance domain. We thoroughly understand insurance company structures, data processing requirements, traditional accounting and regulatory reporting compliance and evolving technology capabilities. We have experience participating in large-scale actuarial and finance transformation journeys and designing financial control framework and closing processes for leading global insurance companies. EXL partners with clients on their end-to-end IFRS 17 journey, helping them achieve compliance, driving greater synergies within the business, and providing managed service solutions.

EXL doesn’t stop at providing implementation support; we have been a known insurance industry service provider assisting multiple clients in their journey from project implementation, BAU design and set up, to operationalising a full-functioning BAU state. Our full range of services and multiple skillsets provide project continuity, while delivering cost efficiencies through such considerations as shared services and right-shoring models.

To learn more or to engage us on your IFRS 17 journey, please visit www.exlservice.com today.

Written by

Ravi Bhanot

Sr. Consultant,

Insurance Consulting, EXL

Swati Hazare

Sr. Consultant,

Finance Insurance Consulting, EXL

Key Contributions:

Ashish Gupta

Assistant Vice President,

Insurance Consulting, EXL

Prashant Chaturvedi

Vice President,

Head of Finance Transformation/ F&A (UK, Europe), EXL