Intelligent Remote Property Assessment

Intelligent Remote Property Assessment

Property risk assessment is an essential process within the property and casualty (P&C) industry that has been largely unaffected by technological disruptions – until now. The use of image analytics and AI can transform end-to-end processes by providing powerful location intelligence that makes property risk assessment precise and simple -- with minimal manual intervention.

Read the latest white paper to learn how image analytics can help insurers:

- Enhance underwriting with granular location intelligence and digital property inspections

- Accelerate claims settlement and improve the customer experience

- Streamline policy renewals with automated triggers and alerts

- Leverage property attributes and risk insights for targeted marketing

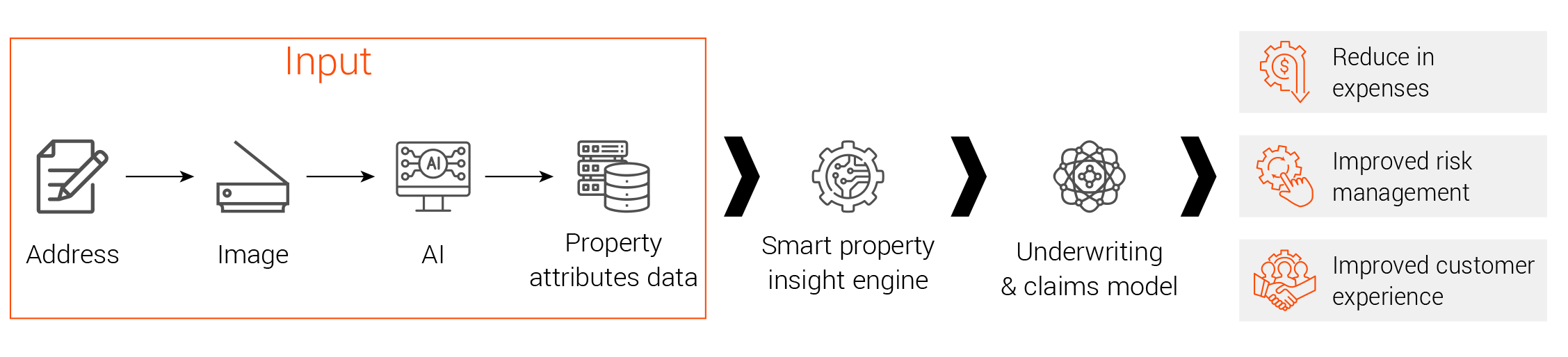

The right image analytics approach offers increased visibility, lower loss ratios, and reduced operational expenses by extracting property attributes from multiple geo-spatial data sources and combining them with streamlined analytics workflows. The diagram below provides a high-level view of an impactful image analytics practice: