Dispute operations are under increasing pressure from rising transaction volumes, faster payment cycles, and stricter regulatory expectations. At the same time, fraud-related losses continue to grow. The Nilson Report projects that global card fraud losses will exceed $40 billion annually in the coming years, placing additional strain on already complex dispute processes.

The impact extends beyond cost. Poor service and friction in customer interactions can drive significant churn, particularly in high-stakes moments such as fraud and dispute resolution. When customers are asked to repeat information or wait for unclear outcomes, what should be a moment of reassurance becomes a point of frustration.

Despite this, many banks still rely on fragmented systems, manual workflows, and inconsistent decisioning. A single dispute can require navigating dozens of systems, while customers are often contacted multiple times to provide missing information. These inefficiencies increase costs, extend resolution timelines, and introduce variability into outcomes.

Traditional automation and assistive AI have improved parts of the process, but they have not addressed the core challenge of executing dispute resolution end to end with consistency, speed, and accountability.

Agentic AI introduces a new approach by embedding decisioning, execution, and control directly into dispute workflows. This allows banks to move from fragmented processes to coordinated, outcome-driven operations, where automation and human judgment are applied in the right places. The result is faster resolution, lower cost-to-resolve, and more accurate, consistent decisions, delivered with full auditability and governance.

The breaking point in dispute operations

Dispute resolution has always required coordination across multiple systems, stakeholders, and regulatory frameworks. What has changed is the speed and scale at which these processes must now operate. Customers expect near-immediate responses and disputes settled faster, while regulators require full traceability across every decision.

In this environment, inefficiencies can compound quickly. Resolution timelines extend, costs increase with volume, and outcomes vary depending on individual interpretation. What was once a manageable back-office process has become a high-stakes operational and customer experience challenge.

Why traditional approaches have not closed the gap

Automation and AI have delivered incremental improvements, but the underlying model remains unchanged. Rule-based automation handles structured tasks but struggles with exceptions. Assistive AI can guide decisions but still depends on human agents to interpret, coordinate, and execute across systems. In both cases, orchestration remains manual.

This leads to large operational teams, ongoing training requirements, and inconsistent outcomes. The challenge is not a lack of intelligence, but the absence of a system that can translate that intelligence into coordinated, governed execution across the full dispute lifecycle.

Agentic AI and the shift to executable operations

Agentic AI represents a shift from decision support to decision execution. Instead of optimizing individual tasks, it is designed to manage outcomes. It can plan, sequence, and execute multi-step workflows across systems while operating within clearly defined governance boundaries.

In practice, this means that dispute operations can be redesigned around a coordinated, end-to-end process rather than a collection of disconnected activities. Decisions are applied consistently based on codified policy, actions are executed automatically where appropriate, and exceptions are escalated intelligently for human review. Every step in the process is recorded, creating a complete and auditable trail.

This does not eliminate the role of human expertise. Instead, it repositions it. Human agents focus on complex, high-risk, or ambiguous cases where judgment is required, while routine and rules-driven work is handled autonomously. Over time, as confidence in the system grows, banks can expand the scope of automation within clearly defined thresholds.

Redesigning the dispute lifecycle around agentic AI

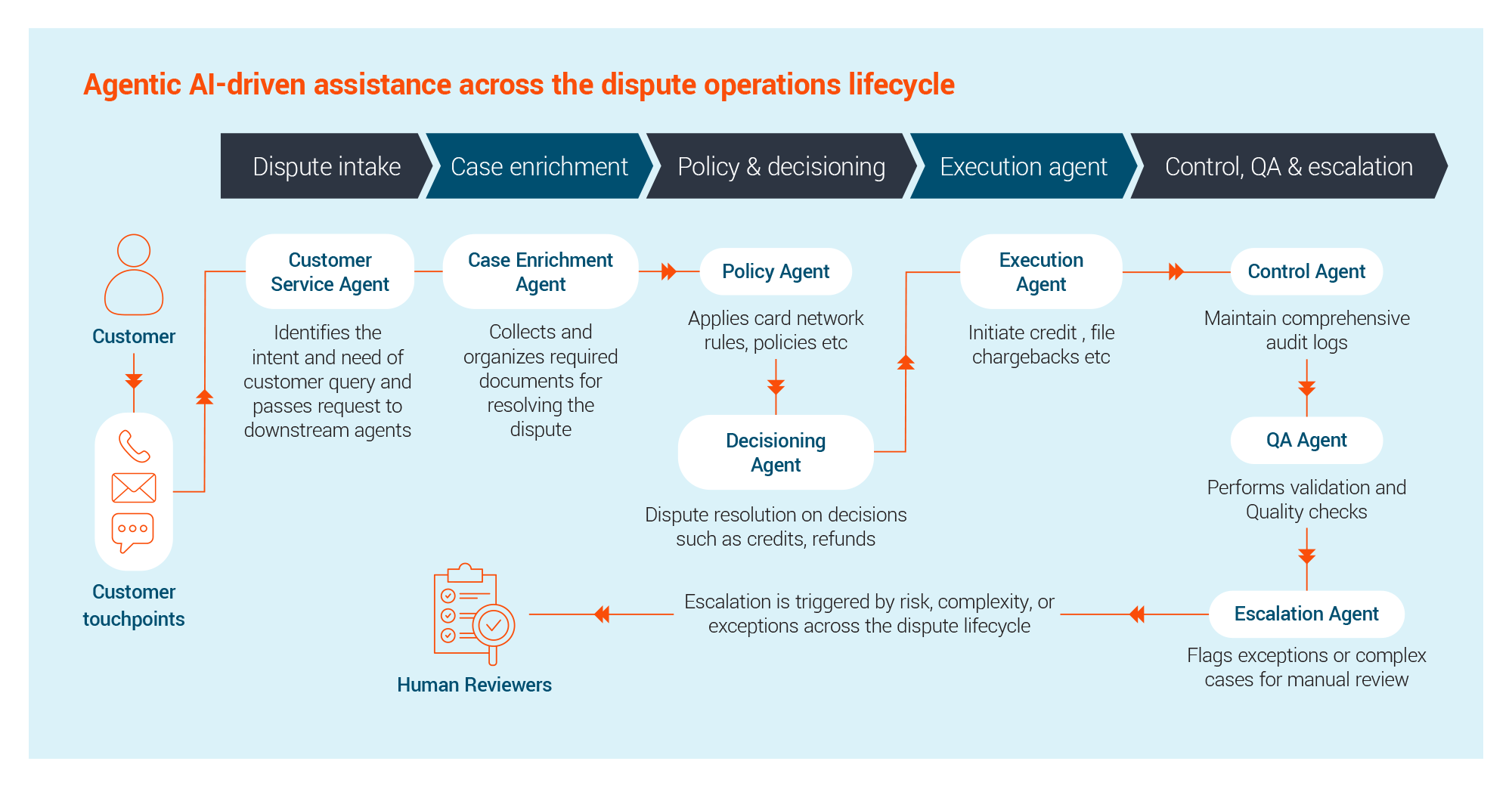

Rather than treating dispute resolution as a series of disconnected steps, agentic AI enables a coordinated process in which data, decisions, and actions flow together.

Intelligent intake and case creation

The process begins at intake, where the quality of information captured determines how efficiently a case can be resolved. Incomplete intake often leads to delays and repeated customer interactions. An agentic approach guides structured intake, validates eligibility in real time, and ensures that all required information and evidence are collected upfront, reducing rework and accelerating time to first action.

Case enrichment and evidence assembly

Once a case is created, the next challenge is assembling the information required to investigate it. Traditionally, this involves navigating multiple systems and manually building context.

Agentic AI consolidates this process by aggregating transaction data, historical disputes, device and IP information, and policy inputs into a single case view. Missing data is identified early, allowing investigations to begin with a complete and consistent picture.

Policy-driven decisioning

Decisioning is governed by card network rules, regulatory requirements, and internal policies. Applying these consistently at scale has been difficult when dependent on individual interpretation.

By codifying these rules, agentic AI ensures that outcomes such as eligibility, provisional credit, or rejection are applied uniformly. Each decision is supported by a clear rationale, making it explainable and auditable.

Automated execution

Execution is often where dispute processes slow down. While some cases require human oversight, many actions such as filing chargebacks, issuing credits, updating systems, and submitting cases to network portals can be triggered automatically once a decision is reached. This reduces delays, minimizes manual error, and removes operational bottlenecks.

Overall, an agentic-driven dispute lifecycle model has the potential to change the speed and economics of dispute resolution. By removing handoffs and enabling parallel processing, agentic AI compresses cycle times and improves responsiveness. High-volume, lowcomplexity cases can be resolved with minimal human intervention, reducing cost-to-serve and training overhead, while standardized decisioning and embedded governance improve accuracy and reduce risk.

Consistency, explainability, and governance at scale

Achieving consistent outcomes across large volumes of disputes has long been a challenge. Variability in how policies are applied can lead to errors, increased losses, and regulatory exposure.

Agentic AI addresses this by embedding policy and regulatory logic directly into decisioning. Instead of relying on individual judgment for routine cases, decisions are derived from standardized rules applied uniformly, ensuring alignment with both network requirements and internal risk tolerances.

Consistency must be paired with explainability. Institutions need to demonstrate how decisions are made. By maintaining detailed records of inputs, rules, and actions, agentic systems provide a transparent and traceable view of every case, strengthening compliance and simplifying audits.

This depends on governance being built directly into workflows. Automated decisions operate within defined financial thresholds, risk limits, and policy constraints, with exceptions automatically escalated for human review. Rather than relying on individuals to interpret procedures, control is embedded into the system so that every action is recorded and every decision is traceable.

Clear ownership is equally important. Responsibility for agentic operations must be defined across risk, operations, and technology teams to ensure effective oversight and continuous improvement.

The path forward for banking leaders

Dispute operations are no longer a back-office function. They sit at the intersection of customer experience, financial risk, regulatory accountability, and operational efficiency. As payment ecosystems accelerate and fraud becomes more complex, the limitations of manual and fragmented operating models are becoming difficult to sustain.

The transition to agentic dispute operations should not be viewed as a single transformation program, but a strategic evolution of how work is performed. Leading institutions are beginning with high-volume, low-complexity disputes where automation can deliver measurable value under clear, governance controls. From there, they are expanding into more complex decisioning scenarios such as data integration, oversight frameworks, and operational confidence mature.

Success requires more than technology alone. It demands the ability to integrate across legacy environments, navigate regulatory requirements, and operationalize AI in a way that is explainable, governed, and scalable. Institutions making the greatest progress are combining advanced AI capabilities with deep domain expertise and disciplined execution. For banking leaders, dispute operations are becoming a proving ground for agentic AI. Few functions combine high transaction volumes, complex decision-making, regulatory scrutiny, and direct customer impact in the same way. The organizations that successfully transform disputes will do more than reduce costs and improve service levels. They will establish a blueprint for how AI can be deployed across the broader enterprise.

Agentic AI enables a model in which decisioning, execution, and control are embedded directly into workflows, allowing disputes to be resolved faster, more consistently, and with the level of oversight required in a regulated environment. The opportunity is not simply to modernize dispute resolution. It is to create a new operating model designed for speed, transparency, resilience, and scale.