What customers expect now is what lenders must deliver next

Lenders that win in today’s demanding consumer market will grow on the strength of relevant offers that trigger engagement at the exact right time. Hyper-personalized lending makes it possible by aligning products with customer pricing expectations, specific life events, and real-world behavior. It then delivers those offers where customers are, in the moment and channel they prefer, with basic qualifications managed prior to contact.

Most institutions recognize this shift. Far fewer are equipped to execute it consistently. Many still rely on intricate, multi-stage processes that require regulatory compliance, risk assessment, and cross-functional collaboration. Product development timelines often stretch over years or longer. In contrast, fintechs and neobanks have been able to quickly introduce and scale products leveraging modular technology stacks, accelerated decision-making processes, and rapid deployment capabilities.

Research from McKinsey underscores the situation, citing that three out of four consumers express frustration when experiences are not tailored to them.

Hyper-personalized lending flips that equation. It uses data and analytics to understand customer needs, timing, and eligibility with greater precision. It then orchestrates product, credit, and marketing decisions within a connected system. The payoff is not just better response, it is stronger product stickiness, increased share of wallet, and a clear role for the bank as a partner in financial well-being, not simply a seller of credit.

This paper explores how sophisticated analytics and a modular framework can significantly accelerate the launch and scaling of a relevant, multi-product portfolio for fintechs and neobanks.

Why hyper-personalized lending is an urgent need now

The risk of waiting is not abstract. Competitive pressure is accelerating on multiple fronts:

- Digital-first institutions continue to set new expectations for speed and experience.

- Fintechs position themselves as more contextual and responsive than legacy banks.

- Non-bank brands embed financial experiences directly into customer journeys.

When a competing product delivers better-timed, more contextual value, customers move share of wallet. With mature technology, advancing skill sets, and rising customer demand, hyper-personalized lending is no longer a future concept. It is becoming a practical differentiator that can connect data, decisioning, and delivery into a coherent operating model.

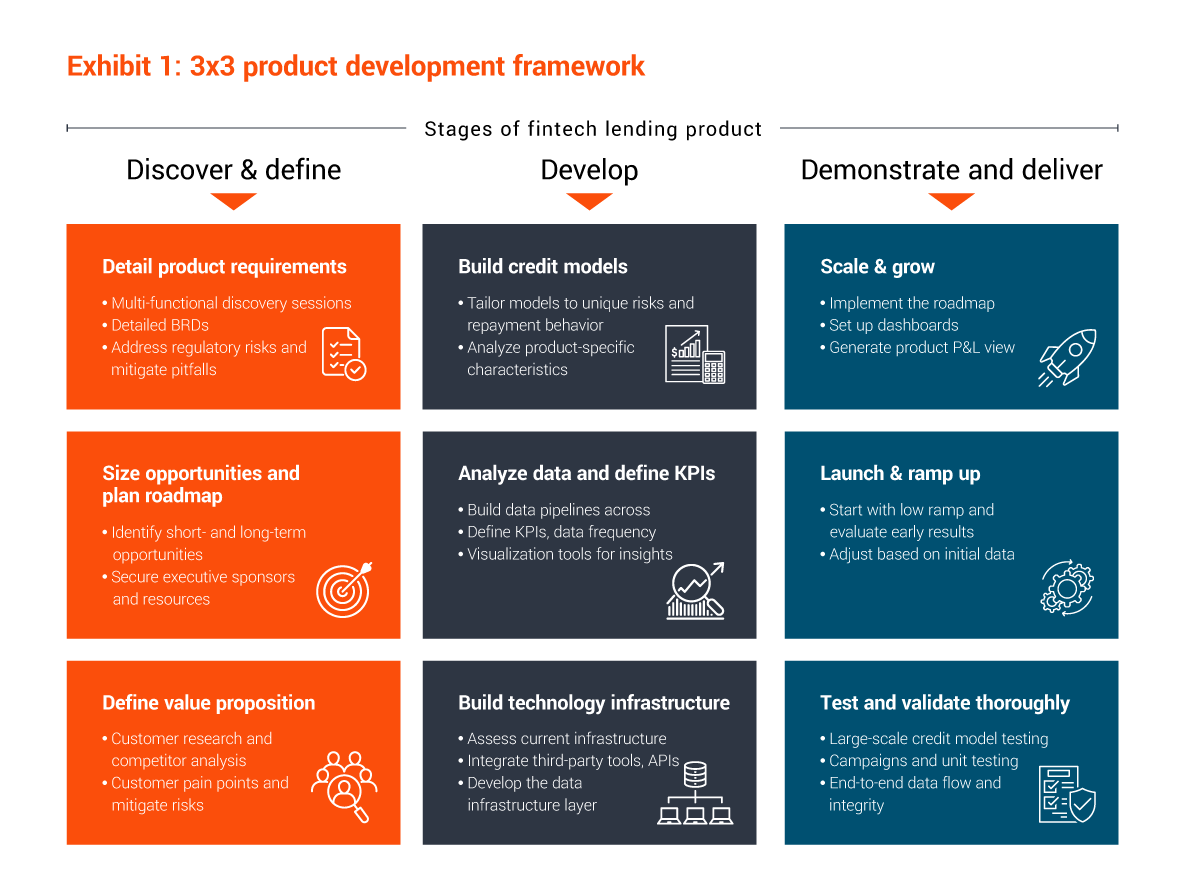

The 3x3 framework for building and scaling products

To operationalize hyper-personalized lending with speed and precision, EXL’s 3x3 product strategy and development framework simplifies workflows, reduces internal confusion, and creates an execution path that supports multi-product portfolios. The framework is organized across three stages, including discover and define, develop, demonstrate, and deliver. At each stage, clear building blocks drive the framework.

Discover and define: Start with value, not features

Define the value proposition. Hyper-personalized lending starts by identifying a real customer problem worth solving. That requires customer research and competitive analysis, with a clear view of pain points and risks. Cross-functional discovery teams led by executive sponsors cognizant of regulatory risks and process pitfalls will contribute greatly to a detailed plan. The goal is not a new product. The goal is a product that improves a defined moment in the customer’s financial life.

Size opportunities and build the roadmap. Opportunity sizing is essential for securing executive sponsorship, funding, and resources. Be wary of intuition-driven estimates and overly simplified models that may carry significant margins of error. As well, overly complex models may be difficult to explain. Avoid layers of assumptions that can undermine business viability. Instead, leverage a combination of internal historical data, benchmarks, macro trends, and market growth projections for a forecasting model that is rigorous enough to trust, yet simple enough to explain.

Exhibit 2: Product opportunity sizing model

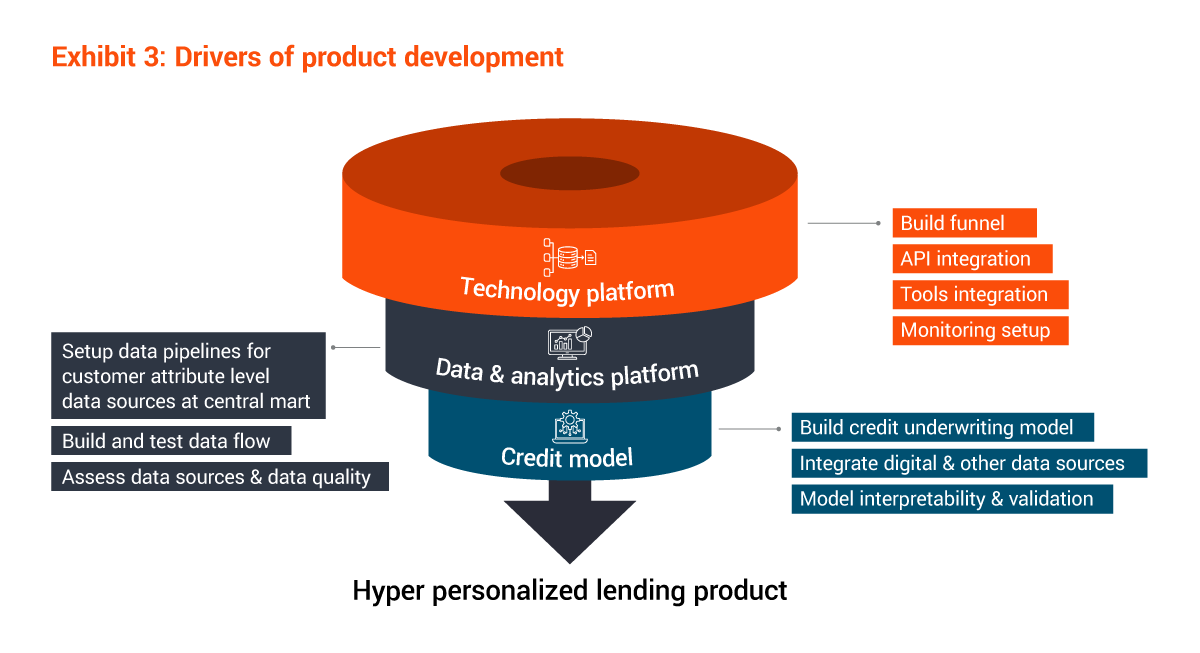

Develop: Build the foundation for speed and scale

The develop stage is where ideas become executable. Business requirements translate into product requirement documents, including architecture, customer flows, and data flows. Existing components should be leveraged where possible to accelerate delivery, but the organization must be explicit about what changes are required to support launch and long-term scale. Build the technology infrastructure. Development begins with an assessment of current infrastructure and the resources required to build and launch. Functions may be at different maturity levels, which can create uneven readiness across the program. A modular approach can help teams reuse proven components, as well as integrate APIs, third-parties, and marketing technology tools to build the data infrastructure needed for both initial launch and future scale.

Establish the data and analytics foundation. Hyper-personalized lending depends on trustworthy data. Focus on centralized integration, storage, processing, governance, and accessibility to ensure a reliable and secure analytics foundation. Socialize KPIs early, including measurement techniques, and follow a test-and-learn setup for use across the product lifecycle. Use visualization tools to improve decisions and gain insight into what should be measured and how often.

Build credit models with product-specific nuance. Building underwriting models from scratch is time- and resource-intensive. For best results, build on proven models, tailoring them to product-specific risk characteristics and repayment behavior. Explore alternative data, such as digital transfer networks and customer engagement footprints, to refine the model for your specific product and customer context.

Demonstrate and deliver: Reduce risk, then ramp with confidence

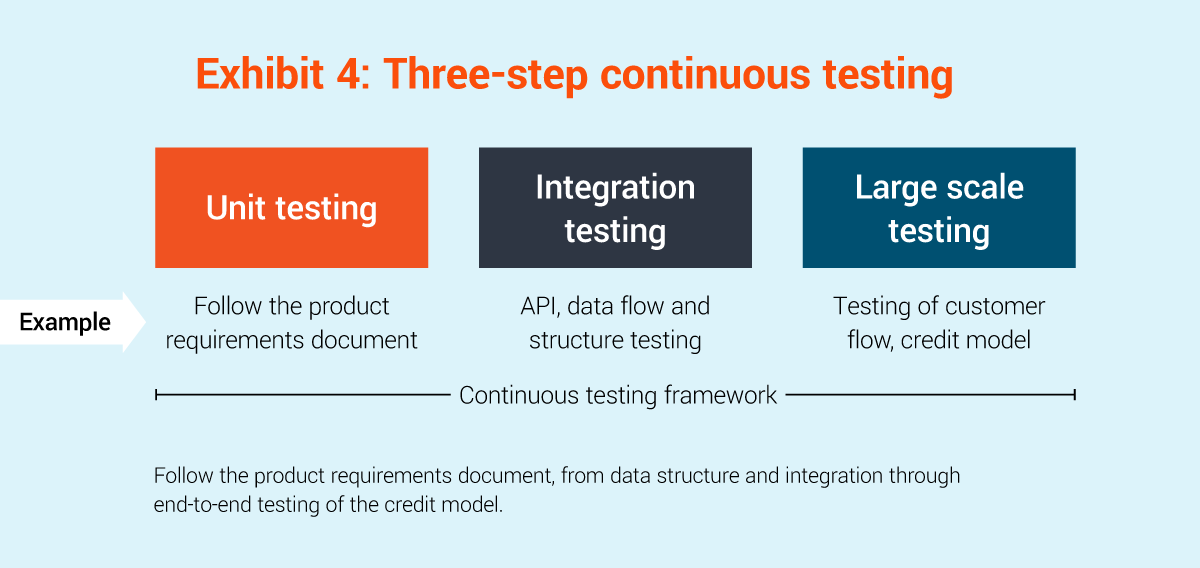

Hyper-personalized lending requires execution discipline. A launch that fails can damage customer trust, create regulatory exposure, and consume scarce capacity through rollbacks and production fixes. At the same time, testing cannot become a reason to delay indefinitely. To streamline delivery, use a three-step, continuous, agile testing approach to ensure minimal rework, precise testing, and error-free rollouts and ramp-ups.

Test and validate thoroughly. Testing should cover technology infrastructure and data layers, underwriting model behavior, and campaign setup quality, with emphasis on end-to-end integrity versus isolated component success. Include unit testing, integration testing, and large-scale testing, supported by a continuous testing framework, for best results.

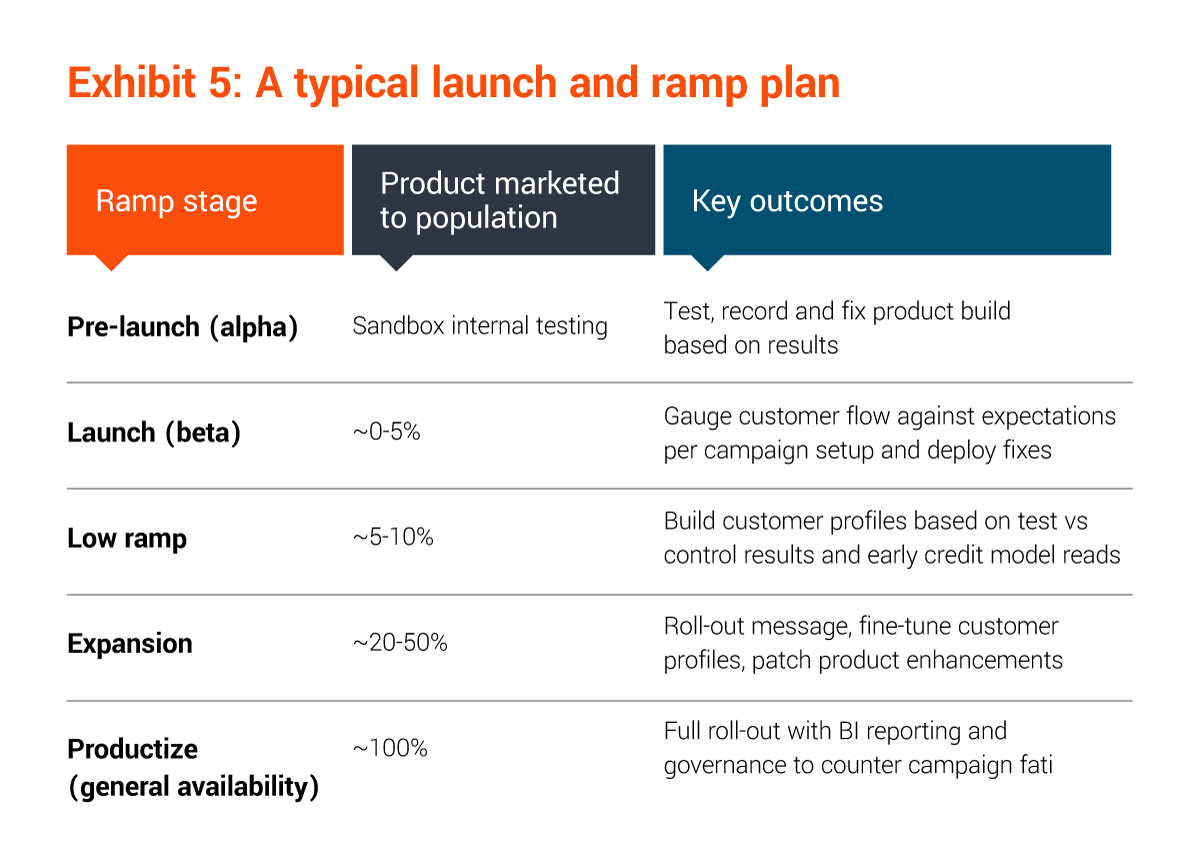

Launch and ramp with a low-and-grow strategy. Large launches can create buzz, but they also amplify risk. Lending launches are especially sensitive due to regulatory obligations, customer service readiness, investor demand, and delinquency management. Start low and grow slowly. Using a controlled ramp, evaluate early results, recalibrate messaging and campaign setups, revisit the credit model to improve profile inflows, and mitigate response fatigue and cannibalization as scale increases. Exhibit 5: A typical launch and ramp plan

- Pre-launch (alpha) -> Sandbox internal testing->Test, record and fix product build based on results

- Launch (beta)->~0-5%->Gauge customer flow against expectations per campaign setup and deploy fixes

- Low ramp->~5-10%->Build customer profiles based on test vs control results and early credit model reads

- Expansion->~20-50%->Roll-out message, fine-tune customer profiles, patch product enhancements

- Productize (general availability->~100%->Full roll-out with business intelligence reporting and governance to counter campaign fatigue

Scale and grow with visibility and governance. Scaling requires more than a marketing budget. It takes a comprehensive playbook, with business intelligence reports, dashboards, and a product P&L views to track engagement and performance, guide enhancements, and sustain value over time.

Expect greater engagement, stickiness, and share of wallet

Hyper-personalized lending changes the customer experience and the institution’s economics.

From the customer perspective, the experience becomes more relevant and more confidence-building. Instead of receiving generic invitations to apply, customers receive outreach aligned to life stage, needs, and eligibility. In practical terms, that can mean engaging pre-approved customers with a message that reduces friction and uncertainty.

From the institution’s perspective, the biggest shifts include:

- Higher resonance and stronger product stickiness.

- Improved share of wallet.

- Greater customer loyalty.

- Less wasted outreach and better timing.

- A more trusted role in financial well-being.

The relationship shifts from selling products to helping customers make confident choices that fit their circumstances.

Overcoming the obstacles

In practice, three challenges arise:

- Inertia in traditional functions. Teams have established workflows and handoffs, and moving from tried-and-true methods can feel riskier than maintaining the status quo.

- Workflow redesign across functions. Hyper-personalized lending depends on coordination between product, risk, data, analytics, and marketing, not sequential effort. That requires new collaboration patterns and clear ownership.

- Modern tooling and capabilities. Many institutions need more data-oriented, customer-focused tools to support real-time insight and orchestration.

A realistic path forward does not require rewriting the organization overnight. The most effective approach is modular. Identify the functional building blocks required for the product, build those modules in sequence, and stitch them together into an end-to-end capability. This reduces disruption while maintaining forward momentum. It also replaces internal chaos with a clear roadmap and shared framework all stakeholders can agree on.

Take the next step with EXL

Hyper-personalized lending is quickly becoming the standard for relevance in a rapidly changing market. Digital banks, neobanks, and fintechs that act now will be better positioned to protect relevance, grow engagement, and expand share of wallet as competition increases.

EXL helps organizations move from intent to execution with a modular product framework, deep fintech and banking domain experience, and cloud-based AI solutions designed to plug into key stages of the implementation journey. The result is a clearer roadmap, faster go-to-market execution, and a more scalable path to building a multi-product, hyper-personalized lending portfolio.

To explore what hyper-personalized lending could look like in your environment, reach out to EXL today.